If you’re looking for the PPV per unit, divide the total PPV by the number of units purchased by your business. To determine the total PPV for a specific order, subtract the standard amount from the actual amount. If feasible, at the end of every reporting period an analysis of purchase and production costs for capitalizability should be performed. You can calculate the standard quantity of materials by multiplying the standard quantity of materials per unit of output by the actual units of output produced in a given period.

Favorable Material Quantity Variance

- The first step in activity-based variance analysis is to assign all overhead costs to a level of activity.

- Sharing variance reports and findings with relevant departments fosters a collaborative environment where everyone is aware of cost control objectives.

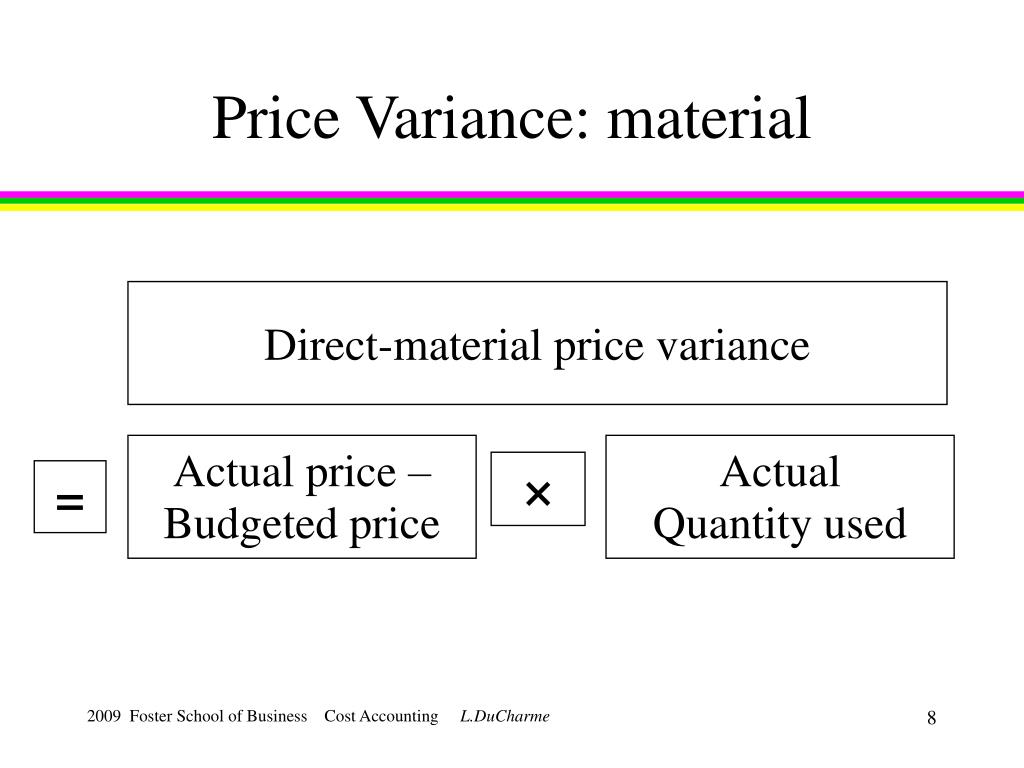

- The material quantity variance is also known as the material usage variance and the material yield variance.

- Mark P. Holtzman, PhD, CPA, is Chair of the Department of Accounting and Taxation at Seton Hall University.

Conversely, a parsimonious standard allows little room for error, so there is more likely to be a considerable number of unfavorable variances over time. Thus, the standard used to derive the variance is more likely to cause a favorable or unfavorable variance than any actions taken by the production staff. Angro Limited, a single product American company, employs a proper standard costing system. The normal wastage and inefficiencies are taken into account while setting direct materials price and quantity standards.

Question 1

As businesses strive for greater precision in cost management, advanced techniques in variance analysis have become increasingly valuable. One such technique is the use of trend analysis, which involves examining variance data over multiple periods to identify patterns and trends. By understanding these trends, companies can anticipate future variances and take proactive measures to mitigate them. Analyzing direct material variance is a powerful tool for businesses aiming to maintain cost control and enhance profitability. By delving into the specifics of variances, companies can uncover inefficiencies and make informed decisions to optimize their operations. The first step in this analysis is to regularly review variance reports, which provide a snapshot of how actual costs compare to standard costs.

Additional Business & Financial Calculators Available

The purchase price variance is the difference between the standard costs for the material and landed cost elements and the corresponding actual costs from the matched, posted, and extracted vouchers. Based on the timing of the voucher processing and the Landed Cost Extract process, the PPV could be computed and posted in one or two parts. If the voucher is not available when you run the Transaction Costing process, then the system calculates the difference between the standard cost and the PO price.

He has served in various leadership roles in the American Bar Association and as Great Lakes Area liaison with the IRS. Take self-paced courses to master the fundamentals of finance and connect with like-minded individuals. Our goal is to deliver the most understandable and comprehensive explanations of financial topics using simple writing complemented by helpful graphics and animation videos.

Knowledge of this variance may prompt a company’s management team to increase product prices, use substitute materials, or find other offsetting sources of cost reduction. In a multi-product company, the total quantity variance is divided over each of the products manufactured. Lumber costs may rise due to increased fuel costs and then lower when diesel prices stabilize. In food service, the price of ingredients, such as milk and eggs, is always changing. When your business purchases others goods to produce your products, you must incorporate the cost of the supplies into your budgets at the beginning of the year and each month.

It also helps identify inefficiencies within the supply chain or production process that may otherwise go unnoticed. Now that we have understood the direct material price variance calculation, let’s look at how to interpret it. Learn how to calculate, analyze, and apply direct material variance for effective cost control and improved financial performance. Finance Strategists is a leading financial education organization that connects people with financial professionals, priding itself on providing accurate and reliable financial information to millions of readers each year. The material quantity variance is also known as the material usage variance and the material yield variance. Of course, variances can be caused by production snafus, such as an excessive amount of scrap while setting up a production run, or perhaps damage caused by mishandling.

He has been the CFO or controller of both small and medium sized companies and has run small businesses of his own. He has been a manager and an auditor with Deloitte, a big 4 accountancy firm, and millions of americans might not get stimulus holds a degree from Loughborough University. A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation.

Leave a Reply